- US equities have continued to hit fresh highs, perhaps suggesting that investors may be too complacent about expanding valuations.

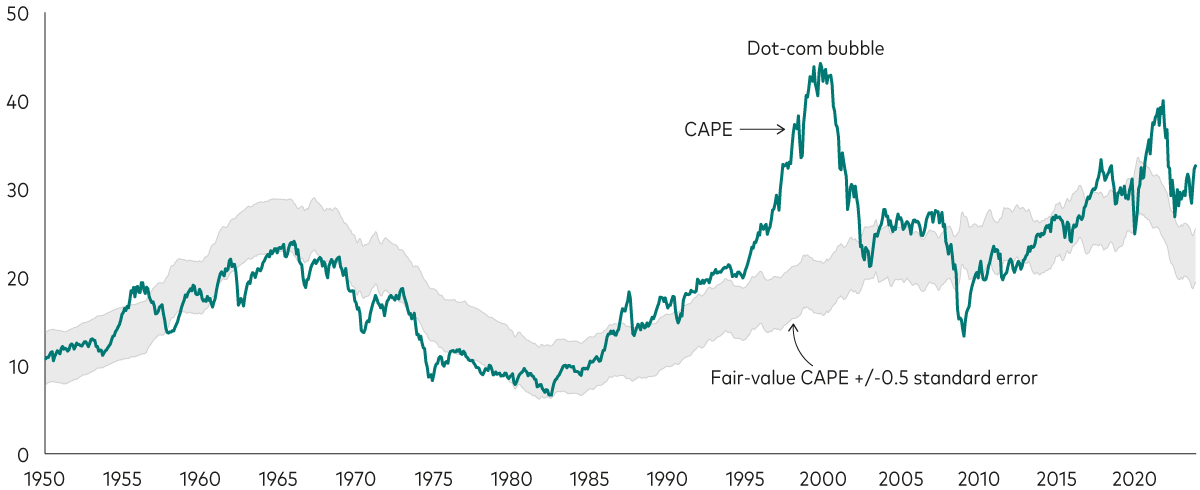

- By our analysis, valuations have only been this high twice since 1950: during the dot-com bubble and during the Covid-19 reopening.

- In this environment, a diversified investment approach remains an effective approach to dealing with potential market volatility.

Higher interest rates can be a headwind for asset prices. The US bond market has adjusted to them, as reflected in bonds’ sharp price drops over the past two years. The equity market, on the other hand, has continued to hit fresh highs, suggesting investors may be too complacent about expanding valuations.

Where US equity valuations stand today

Valuations, or the market’s view on how much companies are worth, are looking a bit frothy. The chart below shows a common metric for valuing the US equity market, the cyclically adjusted price/earnings (CAPE) ratio. To smooth out the impact of economic cycles, it considers current share prices in the context of 10-year inflation-adjusted earnings per share. In January 2024, the CAPE ratio for US equities was more than 30, higher than in most periods of the past 70 years.

But what we think of as fair value for equities depends in part on the macroeconomic environment, including interest rates, inflation and market volatility. Higher stock market valuations can be justified during periods of low interest rates, low inflation and low volatility. The low rates push down the discount rate and the cost of a stake today in a company’s future earnings.

US equity prices have climbed to new highs even as the transition to a higher interest rate environment has depressed our estimate of where fair value lies. The widening gap between equity prices and our assessment leaves the US equity valuation about 30% above our estimated range of its fair value.

For context, US stock valuations have rarely been this high. Their valuation today is at the 99th percentile, a level matched since 1950 only by the dot-com bubble and the post-Covid-19 reopening – as seen in the chart below.

How the valuation gap could close over time for US equities

A fall in interest rates could help close the valuation gap. However, we foresee the Fed remaining cautious. Faced with the prospect of inadequate progress in the inflation fight and the risk of financial conditions easing too rapidly, it is possible that the Fed won’t be able to cut interest rates this year. In the event policy rates are cut this year, we don’t expect them to be enough to significantly increase our fair-value estimates. Beyond 2024, the fair-value range is unlikely to revert to levels that prevailed at the start of the decade. The era of near-zero interest rates is behind us.

It’s much more likely that the gap would close through falling equity prices.

The risk of a correction in equity prices has risen as valuations have become more stretched

Notes: Vanguard’s US fair-value CAPE is based on a statistical model that adjusts CAPE measures for the level of inflation and interest rates. The statistical model specification is a three-variable vector error correction that includes equity-earnings yields, 10-year trailing inflation and 10-year US Treasury yields estimated from January 1940 to January 2024. Details were published in the 2017 Vanguard research paper Global Macro Matters: As US Stock Prices Rise, the Risk-Return Trade-off Gets Tricky. A declining fair-value CAPE suggests that higher equity-risk premium (ERP) compensation is required, whereas a rising fair-value CAPE suggests that the ERP is compressing.

Sources: Vanguard calculations, based on data from Robert Shiller’s website, the US Bureau of Labor Statistics, the Federal Reserve Board, Refinitiv and Global Financial Data.

What equity valuations can and can’t tell us

Valuations are a strong indicator of long-term equity returns. And that doesn’t bode well for the US equity market given where valuations currently sit.

We would caution, however, that while valuations are undoubtedly high right now, that doesn’t mean they can’t go higher, especially in the near term. Valuations are not a market-timing tool. And even over extended periods, valuations are not infallible predictors of outperformance or underperformance.

That’s why, even with our more guarded outlook for US equity returns over the next decade, we would not encourage investors to make drastic changes to their asset allocation.

Diversification is the healthy option when equity valuations are stretched

Regardless of the return outlook for US equities, having a mix of assets that are not perfectly correlated helps reduce risk in a portfolio. Just as living a balanced life is conducive to good health, finding balance in an investment portfolio gives investors a healthy chance of achieving their long-term financial goals.

There may yet be further volatility in markets in 2024, given the transition to a higher interest rate environment is not yet complete. But patient multi-asset investors, who maintain discipline with a strategic allocation to global equities and bonds, are likely to be rewarded over the long term. Furthermore, because it is challenging to time financial markets, we believe investors should stay the course and maintain a long-term perspective to have the best chance of investment success.

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Important information

For professional investors only (as defined under the MiFID II Directive) investing for their own account (including management companies (fund of funds) and professional clients investing on behalf of their discretionary clients). In Switzerland for professional investors only. Not to be distributed to the public.

The information contained herein is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information does not constitute legal, tax, or investment advice. You must not, therefore, rely on it when making any investment decisions.

The information contained herein is for educational purposes only and is not a recommendation or solicitation to buy or sell investments.

Issued in EEA by Vanguard Group (Ireland) Limited which is regulated in Ireland by the Central Bank of Ireland.

Issued in Switzerland by Vanguard Investments Switzerland GmbH.

Issued by Vanguard Asset Management, Limited which is authorised and regulated in the UK by the Financial Conduct Authority.

© 2024 Vanguard Group (Ireland) Limited. All rights reserved.

© 2024 Vanguard Investments Switzerland GmbH. All rights reserved.

© 2024 Vanguard Asset Management, Limited. All rights reserved.